[ad_1]

ideeone/iStock via Getty Images

Before we go any further with this article, we want to dispel the notion that a micro-cap company, with limited resources, has a snowball’s chance in hell of competing with the behemoths already entrenched in a mature industry.

We offer the following for consideration by investors.

For years, the energy drink space was dominated by two primary brands, Red Bull and Monster. Those two companies had a stranglehold the market, and as a result left in their wake a plethora of promising young entrepreneurs who had visions of being able to compete for market share.

The number of failed energy drink brands considerably dwarfed the relatively few number of successes, and it was thought that nobody could snatch the crown away from these two energy drink icons.

Then in 2004, a company named Celsius Holdings, Inc. came along with their version of an energy drink that was not only healthy, but also tasted great.

We won’t take investors through the long and storied history of the company, but simply point out that when we discovered CELH, and began writing the first of some 43 articles on the company, the shares were less than $0.50 cents.

As you can imagine, we were relegated to the ranks of being considered penny stock promoters engaged in some sort of pump and dump scheme.

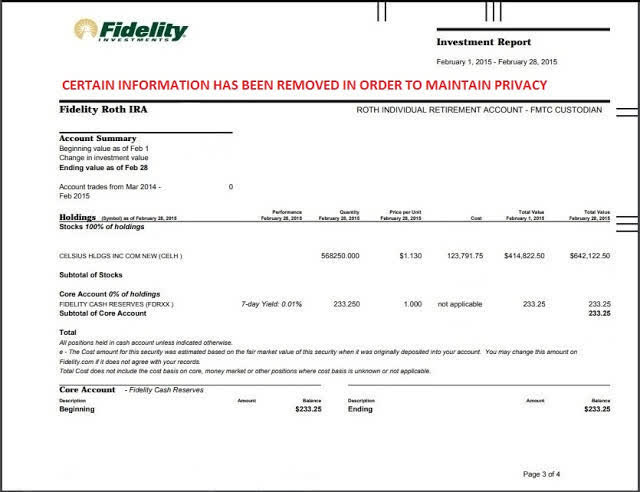

Over the years, we built a huge position in CELH, at one time owning 568,250 shares at an average price of $0.22 cents in February of 2015.

Screenshot February 28 2015 Fidelity Statement

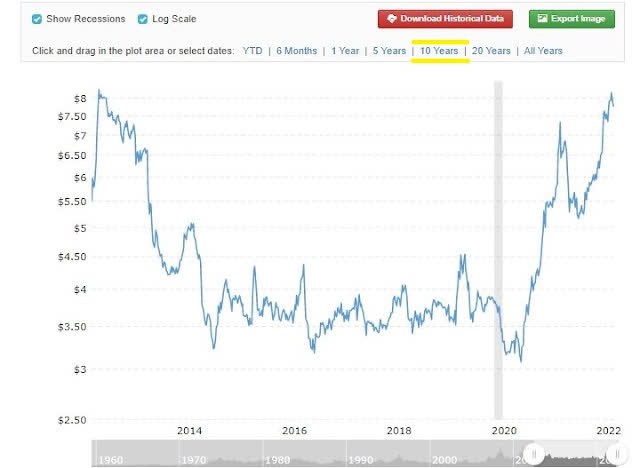

On November 8, 2021, just a little over six months ago, Celsius Holding’s shares hit an all-time high of $110.22. Today, shares rose as much as 29% on the back of blowout numbers for Q1 of 2022.

Now, we would like to tell you that we held every single one of those CELH shares until the price reached $100, but the reality is that we scaled out and sold many of those shares long before the stock took off into the stratosphere, as it went parabolic in price.

We certainly have no regrets, and often will hold a core position, while trading a smaller number of satellite shares. We also encourage micro-cap investors to recover their cost basis whenever possible and hold on to the remaining shares that have virtually little or no cost.

So much for tiny micro-cap companies not being able to compete successfully with the big boys of American enterprise.

We would like to reiterate, as we always do, that micro-cap stocks are considered extremely speculative. Micro-cap stocks carry additional risks beyond those of higher classes of securities including, but not limited to trading outside of a listed exchange, potential liquidity issues, dealing with penny-stock rules, lack of margin eligibility, a possible absence of transparency regarding BBBO quotes, a limited number of Market Makers willing to provide depth to the order book, potential issues regarding financing activities, inadequate capital to execute on the company’s business plan, going concern caveats, and the potential inability to compete with larger companies due to limited financial and personnel resources. Please invest responsibly. We encourage individuals to only invest what they can afford to lose, up to a maximum of 100% of their investment.

Also, please do not assume that the success that we had investing in Celsius Holdings, Inc. (CELH) will be repeated. We merely use CELH as an example of how a micro-cap company can compete with much larger competitors in their industry. Celsius Holdings, Inc. was a unique situation and does not represent the typical outcome of investing in high-risk micro-cap securities.

Now, let’s discuss Blue Biofuels, Inc. (OTCPK:BIOF).

In early March of 2021, we penned a piece named Inflation And Soaring Prices Make Corn Ethanol Unprofitable; Blue Biofuels Offers An Alternative.

At that time corn prices were hovering around the $4.75 to $4.98 price per bushel. Today, the price of corn per bushel stands at $7.75; an increase of 55% in just a little over a year.

The Last 10 Years of Corn Prices 2012 -2022 (Macrotrends)

Source: Macrotrends

Historical Annual Data For Corn Prices 2014 – 2022 (Macrotrends)

Source: Macrotrends

The notion that the Federal Reserve was diligent in monitoring inflation data is almost laughable, as a 5th grader could have probably seen where prices were heading by simply looking at a chart representing a basket of commodities over the past two years.

This past week, we wrote a blog piece about our utter disappointment in the Federal Reserve and its MMT monetary policies, along with the “kick the can down the road” mentality over the past 20 years. Yet, President Biden gave Jerome Powell the nod for another four-year term as the Fed Chairman, last November, based on his being confident that

“Chair Powell [and Dr. Brainard’s] focus on keeping inflation low, prices stable, and delivering full employment will make our economy stronger than ever before.”

Speaking before today’s release of March CPI numbers, President Biden had a few things to say with regards to the dramatic increase in energy costs for U.S. consumers.

With regards to cutting high energy prices, Biden said he had “led the world in the largest release of oil from our stockpiles in history,” allowed biofuels in gasoline, and is driving green investment at the same time as near-record domestic crude production.

Source: World News Era

The Bureau of Labor Statistics released the March CPI data prior to the stock market opening this morning, and the numbers revealed a continuing trend of highly elevated prices for many of America’s most highly prized consumer goods; especially food and energy costs.

So much for Powell’s keeping inflation low and prices stable.

We don’t believe that the Fed will be able to tame inflation anytime soon. The genie is out of the bottle, and it is going to take years, not months, to reverse the irresponsible monetary policies of the past. The stock market has entered a new phase and investors will have to adapt to a shift in investor’s sentiment from one of euphoria to one of anguish and discomfort.

We are now in bear market territory and we will likely continue to be in an environment of higher inflation and lower stock prices. The Fed giveth and the Fed taketh away. It’s just that simple.

Get used to investors selling rallies, not buying the dips. That’s the new stock market reality.

If you have been buying the dips in many high-flying technology stocks, over the past six months, you most likely are experiencing quite a bit of pain due to massive drawdowns in your accounts due to Institutional investors selling.

One of the reasons why we like low-priced micro-cap stocks is that, for the most part, they tend to be immune to the ravages of declining account values as Institutional investors dump their holdings.

After all, they get paid on performance and in bear markets most money managers typically perform very poorly.

Energy prices are up substantially, as are most commodity prices and that is a trend that may continue for quite a while. Remember, the adage “Don’t fight the Fed”? They will be busy attempting to combat inflation by raising interest rates, so plan accordingly for lower equity and bond prices.

That said, we do give credit to President Biden for his emphasis on reducing our future dependence on fossil fuels and implementing a long-term policy for the research and development of alternative energy, which includes biofuels, biodiesel and SAF’s (Sustainable Aviation Fuels).

His recent enactment of a policy which will temporarily allow an increase of ethanol blending with gasoline to go from 10% to 15% is a step in the right direction, but much more will need to be done going forward to have a significant impact on lowering energy prices.

Some countries, like Brazil, run on flex fuel combustion engines, where levels of ethanol could run as high as 100%. Most of Brazil’s ethanol production is cellulosic, derived from sugar cane plants and their stover.

We could learn something from the Brazil model for alternative biofuels made from cellulosic materials, if it were not for the corn-based ethanol lobby entrenched in Washington, D.C for the past decade.

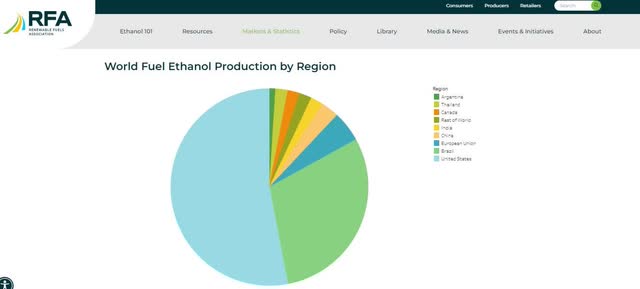

Pie Chart of Ethanol Production by Country – Pie Chart (Ethanol RFA Website)

Source: Renewable Fuels Association

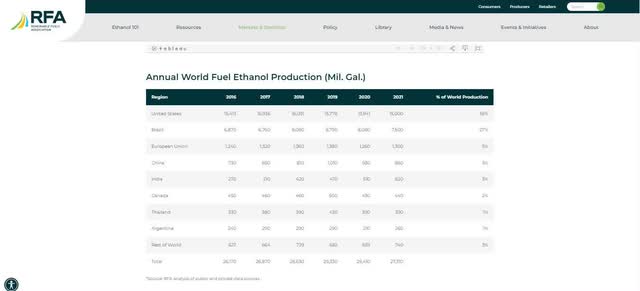

World Ethanol Production by Country – Table View (Ethanol RFA Website)

Source: Renewable Fuels Association

As we opined back in March of 2021, corn-based ethanol production is becoming increasingly costly as the price of corn reaches new highs. This is especially impactful because corn is used for so many of the foods that Americans consume daily.

We also touched upon the ongoing “Food vs. Fuel” debate the has been raging for years.

The use of food crops for the production of 1G biofuels sparked the “food versus fuel” debate. On the one hand, biofuel critics claimed that farmers would sell their crops to higher-paying biofuel manufacturers instead of to their traditional purchasers and thus create food shortages and rapid price increases. On the other hand, supporters asserted that those effects could be attributed to rising costs of petroleum and not to biofuel production. The role of biofuels in global food price dynamics has been the subject of considerable discussion and media attention since 2007. During that debate, cellulosic ethanol emerged as an alternative to 1G ethanol, because it could use waste and non-food plants grown on lower-quality land.

Source: BioRefineries Blog

The traditional use of corn as a feedstock to produce ethanol, carries with it several problems, not the least of which is the increase in the price of corn, as well as those costs associated with fertilizing, planting, mitigating nasty bug infestations and harvesting a seasonal commodity.

Blue Biofuels is currently working with the USDA (U.S. S Department of Agriculture) to optimize the yields of their King Grass feedstock, a perennial grass that the Company is planning to use in their patented cellulose to sugar (“CTS”) process.

The advantages associated with using this King Grass feedstock are numerous and cellulosic ethanol is considered to provide better performance in terms of low risk of direct and indirect land-use change (ILUC) impacts. Because many cellulosic crops are perennial and roots are always present, they guard against soil erosion and better retain nitrogen fertilizer. Most cellulosic sources require much less intensive management than do grain crops, saving the fuel and carbon dioxide costs associated with field crop operations. The climate benefits of cellulosic biofuels derive from two sources: avoided petroleum use (the fossil fuel offset) and GHG mitigation during biofuel production, principally by soil C accumulation and avoided emissions.

Source: BioRefineries Blog

The problem of producing commercial quantities of cellulosic ethanol, at a reasonable cost, has plagued the industry for years. No one has been able to “crack the code” and successfully create affordable cellulosic ethanol and cellulosic-based biofuels…UNTIL NOW

A little micro-cap company, based in South Florida, has been able to develop a promising new technology called CTS 2.0 which converts cellulose biomass to sugar. CTS is the acronym for Blue Biofuel’s proprietary patented Cellulose-To-Sugar process. It could revolutionize the biofuels industry, similar to the way Celsius revolutionized energy drinks.

Under the former CEO and management team, the process, which used a ball mill batch processing method was very slow and inefficient. The company reorganized under Chapter 11 Bankruptcy proceedings in 2018 after a completely new method of processing cellulosic materials was developed which can processes biomass at 99% efficiency within mere minutes.

We wrote our first Seeking Alpha article on Blue Biofuels on January 5th of 2021, which was titled Blue Biofuels Our Absolute Best And #1 Micro-Cap Idea For 2021.

We followed that initial article with two others Blue Biofuels: Why Ethanol Fuel Cells Could Carve Out A Niche In This Super-Hot Sector and Inflation And Soaring Commodity Prices Make Corn Ethanol Unprofitable; Blue Biofuels Offers An Alternative.

We wrote a few pieces on our Google blog page, mostly consisting of minor updates and musings from a technical analysis viewpoint, but in all honesty, there wasn’t a whole heck of a lot to write about.

Until this past week.

On May 4th, after the market close, Blue Biofuels (OTCPK:BIOF) announced that it has partnered with leading machine builder K.R. Komarek to build Blue Biofuel’s CTS reactors, as the company inches closer to commercialization of its revolutionary cellulose to sugar technology.

Investors have been patiently waiting for an update on the progress towards the much-anticipated commercialization of the company’s patented CTS 2.0 technology, and this news appears to forecast that the company will have a 5th generation semi-commercial CTS prototype reactor ready by the end of Summer.

In the company’s 10-Q, released yesterday, they are expecting this 5th generation prototype to produce

approximately one ton per day of the combination of sugar and lignin, which the Company believes will be sufficient to prove the commercial viability of the CTS 2.0 technology. Due to its mechanical nature and modularity, we anticipate that one plant would have multiple modular CTS systems. The Company expects to have a CTS 2.0 modular system ready for commercial production in 12-18 months.

Earlier, in January, the company announced that they had achieved over a 99% conversion rate for a king grass cellulosic material which they plan on using as their primary feedstock.

Blue Biofuel’s CEO, Ben Slager, indicated that this 99+ conversion percentage from cellulosic biomass into water soluble sugars was completed within a reaction time of under one minute.

This will accelerate and solidify the scale-up and commercialization of Blue Biofuels’ patented Cellulose-to-Sugar (“CTS”) process to produce cellulosic ethanol and sustainable aviation fuel, a topic that has seen much support from the current Biden Administration.

Previously, Blue Biofuels announced that it is working with the U.S. Department of Agriculture to optimize the crop yields of Pennisetum hybridum, commonly known as king grass.

Blue Biofuels intends to use King Grass as its primary feedstock in producing these cellulosic biofuels, including SAF (Sustainable Aviation Fuels).

Earlier in the week the company announced that they had filed a Form RW, requesting that the Securities & Exchange Commission withdraw the company’s previously filed S-1 registration statement which was submitted back in February.

Originally, the company had sought to raise capital through investment bank H.C. Wainwright.

The plans outlined in the S-1 included effecting a reverse split of the company’s common shares and up listing the company’s shares to a higher tier of the OTC Markets.

In conjunction with the company’s change in plans, a Form D filing indicates that they intend to raise a much smaller amount of capital through a private network of investors. The terms of the private placement consist of a combination of common stock at a price of $0.15 cents, along with a warrant to purchase additional shares of the company’s common stock through April 27, 2027, at an exercise price of $0.25 cents.

We should note that both Blue Biofuels CEO, Ben Slager, and CFO Anthony Santelli are participating in this current round of financing, making an investment of $75,000 each.

Messrs. Slager and Santelli have filed an SEC Form 4, disclosing their investment in the new offering.

A couple of things stand out to us. First, the fact that the CEO and CFO are participating in the latest private placement is encouraging. Second, the offering which was to be underwritten by H.C. Wainwright has been put on hold.

We have always felt that good corporate stewardship and attentive fiduciary responsibility dictate that any capital market’s offering of substance should be undertaken when there is a price advantage to doing so. In our view, raising a large amount of money at the current stock price level would result in excessive dilution to existing shareholders.

We feel that given the proximity of building a commercial scale reactor (6th prototype), outlined in the press release, it would be best to engage in a capital raise sufficient to meet the urgent short-term capital needs of the company to complete the commercial unit.

Once the engineering and building of the commercial unit is finished, bench-tested and optimized for maximum efficiency and output, only then would the company be able to offer potential investors, or JV Partners, the ability to experience the commercial unit in operation, first-hand.

Depending on the output numbers and the results, the company would be able to forecast how much volume could be produced in a commercial setting, within a given amount of time.

That could then be extrapolated to a produce a revenue forecast, along with the associated costs for things like feedstock, energy usage to run the reactor, labor costs to oversee the production, etc.

These numbers could then be applied to come up with things like gross profit margins and other metrics for management to measure the potential value of the business.

Once a potential valuation has been established, it should be relatively easy to provide interested investors and/or JV Partners with enough information to engage in discussions and negotiations for a much larger capital raise.

In the 10-Q, filed May 11th, the company stated that:

Our goal is to develop our CTS 2.0 technology to a commercial scale and then seek to either enter into a joint venture or acquire existing corn ethanol plants to install the CTS 2.0 technology. The Company is also looking into converting ethanol to sustainable aviation fuel. To minimize dilution to shareholders, we will seek project-based financing to build (or acquire and retrofit) or joint venture with existing ethanol producers to produce cellulosic ethanol and lignin/bioplastics and other specialty chemicals from its patented CTS 2.0 system.

As we indicated earlier, there hasn’t been enough information released by the Blue Biofuel’s management team to warrant writing a follow-up article to our three previous installments on seeking Alpha.

It sounds like they are heading for the home stretch. Whether they will reach the finish line ahead of time, in time, or fall behind again remains to be seen.

As for us, we like an underdog with long odds.

[ad_2]

Source link

More Stories

How To Promote Direct Hotel Bookings

My 50th birthday celebrations in Amsterdam

5 Ways to Improve Hotel Operational Efficiency