[ad_1]

metamorworks/iStock via Getty Images

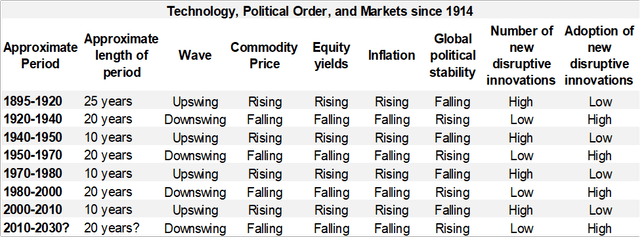

In this series, I have attempted to show that the following chart is a fair summary of the relationship between innovation, war, and markets.

Chart A. The more things change, the more they stay the same. (Author)

This confirms, I argue, the basic (and often misunderstood or misremembered) observations of Nikolai Kondratiev and Joseph Schumpeter a century ago. In Part 1, I outlined the argument. In Part 2, I plotted out the various ways Kondratiev’s Long Waves and Schumpeter’s innovation waves have been (largely) misconstrued since the thinkers died, largely under the pressure of phenomena caused by the transition from one global monetary order to another. I also illustrated how I believe some of my observations untangle many of these misconceptions.

Elsewhere, I have written about how ideological and methodological developments, some of them inspired by Kondratiev and Schumpeter themselves, contributed to a economics-as-engineering approach that led to their observations being regarded as an inconvenience to the serious business of turning economics into a technocratic plaything. In Part 3, I plotted the emergence and diffusion of the last century’s most disruptive innovations-cars, radios, TVs, PCs, and smartphones-and how those patterns match the ones laid out by Kondratiev and Schumpeter.

The primary differences between their observations of gold standard-era patterns and the post-gold standard ones I have outlined in this series is the length of these waves, a shift from nominal prices to real prices, and a transition from producer-oriented disruptions (like railroads) to consumer-oriented disruptions (like smartphones). Under the pressure of a new price regime (or, if you like, a new monetary regime) at the global core, these waves in price, innovation, and political stability have become more frequent since the two Central European economists who documented them died (Kondratiev in 1938 and Schumpeter in 1950).

This brings us to at least two very knotty problems that lie on either side of these observations. The “upstream” problem is causation. How might these phenomena be connected? Does one cause the other? Or are they all generated by some deeper cause, each petals of a single blossom? The “downstream” problem is that of ramifications. Since this is being written primarily for investors on an investing website, we will have to concern ourselves primarily with the ramifications for investment decisions.

Let me begin with one investment ramification in particular.

Technological growth ≠ high returns

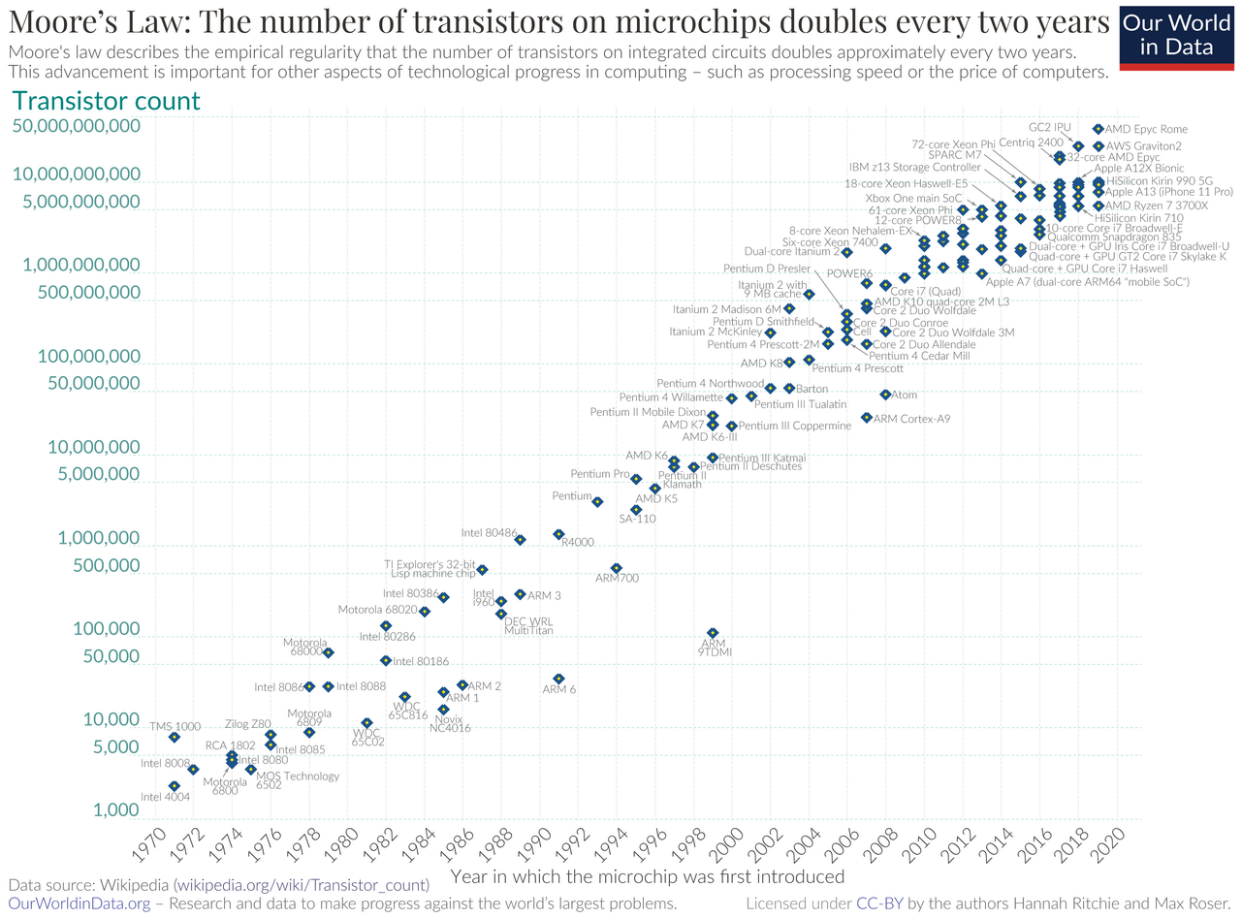

Raw technological power is a poor predictor of short-, medium-, and long-term returns in stocks. Over the very long term, the connection is much stronger, however.

Take one of the most frequently cited technological phenomena, Moore’s Law, first formulated in 1965. The following chart from Max Roser and Hannah Ritchie illustrates the near-constant growth rate in the number of transistors per microchip over the last 50 years.

Chart B. The background rate of technological progress appears to remain constant. (Max Roser and Hannah Ritchie/Our World in Data)

Needless to say, neither stock returns generally nor semiconductor returns in particular show such steady appreciation.

Chart C. Semiconductor stocks do not track Moore’s Law. (Stockcharts.com)

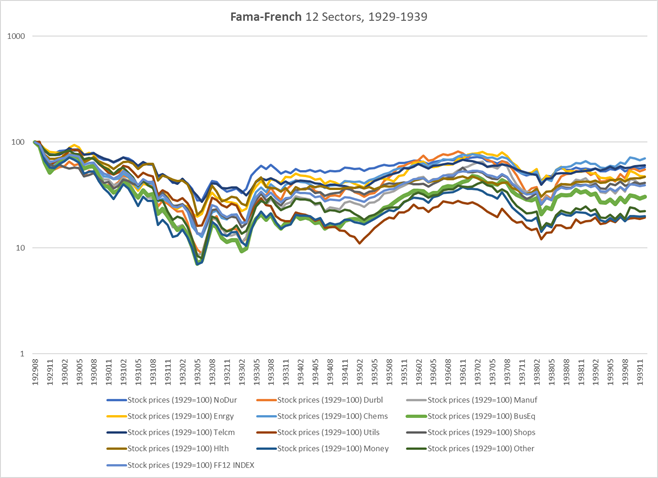

The 1930s are an even better example of this disconnect between underlying technological progress and market returns. As I pointed out in A Primer On Long-Term Sector Rotations And Where We Are Now, the Great Depression was not only the worst bear market in the last 150 years, it was also a period of tech sector underperformance. Even in a deflationary depression, energy outperformed tech. The Business Equipment sector, which is equivalent to today’s Information Tech sector (XLK), is marked by a thick green line in the following chart.

Chart D. Tech stocks were among the worst performers during a period of high technological growth. (Fama-French)

But, this brutal tech bear market occurred during a period of high technological growth.

I am going to rely on Gordon’s characterization in The Rise and Fall of American Growth, which I cited in Part 3, this time to illustrate the amount of technological progress that occurred throughout the Depression. He leaves little room for doubt:

“For every 100 units of electricity that were added to the productive process during 1902-1929, another 230 units were added between 1929 and 1950.”

The “focus on the 1920s as the breakthrough decade misses that the full force of electricity expansion in manufacturing and the rest of the economy took place between 1929 and 1950.”

“The trauma of the Great Depression did not slow down the American invention machine. If anything, the pace of innovation picked up in the last half of the 1930s. This is clear in the data assembled by Alexopoulos and Cohen on technical books published. The dominance of the 1930s…is supported by Kleinknecht’s count of inventions by decade.”

“By 1940, automobile manufacturers had achieved the dream of producing automobiles that could go as quickly as the highways would allow them…”

“[F]rom the discovery of the east Texas oil field to the development of many types of plastics now considered commonplace, the 1930s added to its luster as a decade of technological advance.”

“[T]he Great Inventions of the late nineteenth century, especially electricity and the internal combustion engine, continued to alter production methods beyond recognition not just in the 1920s but in the 1930s and 1940s as well. Alex Field revitalized US economic history by his startling claim that the 1930s were ‘the most progressive decade’.”

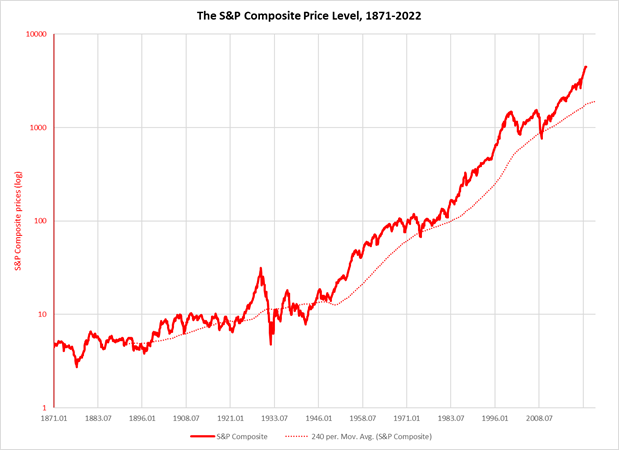

Standing atop the stock market peak in 1929, one could have looked out into the future and seen mountains of technological growth from there to the horizon. Some, like the economist and entrepreneur Irving Fisher, did, and they concluded that stocks would never fall. Some economists today argue that Fisher was essentially right and that stocks in 1929 were undervalued.

Over very long returns, it is extremely likely that technological growth, along with productivity growth (with a bit of help from money printing), results in higher returns.

Chart E. Stocks, over the very long term, appear to be correlated with technological progress. (Robert Shiller)

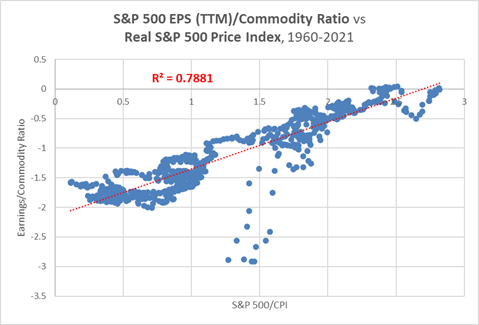

But, the world keeps to its own schedule. Stock returns, like innovations, are bunched together. In the following section, I will attempt to make what has been implicit explicit: stock prices are almost certainly driven by “fundamentals,” but those fundamentals are only barely understood. Just as regular deviations in the expected orbit of a planet implies the existence of an unknown gravitational force, so do the regular deviations from known fundamentals imply the existence of unknown fundamentals. The most obvious example is the relationship between real stock prices and the ratio of earnings per share to commodity prices, illustrated in the following chart.

Chart F. The correlation between stock prices and the earnings/commodity ratio has been rock-solid for decades. (Shiller, World Bank, St Louis Fed)

Macro equity investing ramifications

At its simplest, we can express the relationship between stock prices and Kondratiev Waves in the following equation:

Chart G. The history of market waves suggests that stock prices are driven by the earnings yield, not vice versa. (Author)

The price of a share equals the level of earnings divided by the earnings yield.

In other words, Kondratiev Waves have something to say about only half of what determines stock prices, the P/E ratio (the inverse of the earnings yield). It is silent about the earnings side of the equation. (Mostly silent, I should say, insofar as it appears that earnings growth appears to be both limited by and anticipated by the earnings yield, as I discussed in “The Death of Irrational Exuberance” series).

This formulation, I suspect, is apt to frustrate many readers. The logical assumption might be that the P/E ratio is simply an expression of the ratio of what people happen to be willing to pay at any given point in time for stocks relative to trailing earnings. To that, I can only say that the history of the markets, war, and innovation collude in suggesting that P/E ratios are a distinct phenomenon from ‘P’, price.

Chart H. The relationship between stock prices and the earnings yield changed from the 1920s. (Shiller)

Another way of putting this is that the P/E ratio is more than the sum of its parts. Some have famously tried to argue that P/E ratios are an expression of oscillations between “irrational exuberance” and irrational depression, but again, the connection between the earnings yield and commodity prices, innovation waves, and global political (in)stability suggest that P/E ratios are fundamental in nature, not external or accidental.

What would it mean to place the earnings yield, commodity prices, and the Kondratiev Wave at the center of the pricing universe? Most likely, it would imply the displacement of the role of the autonomous investor (rational or otherwise) in favor of an entity much more complex than modern finance would prefer to posit. To oversimplify things, instead of the classical rational investor or the more contemporary Pavlovian investor, think Freud and Jung: a collection of murky, chaotic, dreamlike, (but evolutionarily-derived) urges spread across a collective unconscious with a thin layer of conscious awareness on top. That is, the investor is both more complex than is modeled and less autonomous.

If we let narrow rationalism be our measure, we will inevitably find that homo economicus appears rational when things work out for the best and hopelessly irrational when things fall apart. We then end up in a Blind Men and the Elephant argument about whether markets are efficient or not, or whether one should rely on fundamentals or technicals.

Let’s add another layer to this. Since the establishment of the Fed in 1914 and especially after the 1940s, the earnings yield has been dominated by the price side of the equation. Earnings have, except for cyclical shocks, grown at a near constant rate since the depths of the Depression while stock prices have orbited around them (as illustrated in the previous chart). But, prior to the establishment of the Fed, stock prices and the earnings yield were rather consistently correlated with one another. Stock prices, earnings, and the earnings yield tended to move together. In times of disinflationary crises, this tendency reemerges (for example, the 1930s and 2008-2010).

Thus, correctly anticipating long-run changes in P/E ratios would have been a profitable trading strategy over the last century, especially if combined with a bit of cyclical agility or, via something like Shiller’s CAPE, cyclical smoothing.

In short, knowing the status of Kondratiev Waves is an essential input to investment decisions but, used in isolation from a correct anticipation of long-term earnings trends and/or the status of the earnings cycle, could be disastrous. If one wanted to rely on a single measure, a simplified measure like Shiller’s CAPE would be a better guide.

Macro commodity investing ramifications

Because commodity prices are at the core of the market side of Kondratiev Waves, this is somewhat more straightforward. Commodity supercycles have occurred every third decade since the 1910s, as illustrated in previous installments. But, the pattern was different before 1914.

In the last century, there have typically two decades of secular bearish trends in commodities followed by a powerful bullish supercycle. But, prior to the establishment of the Fed, the pattern was 25-30 years of secular bearishness followed by secular bullishness for 25-30 years.

If one isolates commodity supercycles from the behavior of the earnings yield, stock prices, earnings cycles, innovation supercycles, and geopolitical conditions, you are left with nothing other than the reliability of the length of a given supercycle. Since the length of these supercycles (which appear to be real) is in part determined by the monetary regime (gold standard vs central banking standard), you have to correctly gauge the stability and durability of a given monetary regime. A brief glance at the history of monetary standards suggests that they are extremely susceptible to political manipulation and, more importantly, hubris. Step by step, the departure from the gold standard was an accident based on an inability to foresee the full array of consequences that would flow from setting up the Federal Reserve. FDR’s and, later, Nixon’s actions were simply recognitions of the reality that had been created by the Fed: there was no longer enough gold to back the dollar.

If you break Kondratiev and Schumpeter Waves into their smallest components, you will make the same mistakes that we documented in Part 2. The interrelationship of the earnings yield (and thus stocks and earnings, as well), commodity prices, innovation waves, political stability, and the monetary system is the fundamental fact of these Waves while their cyclicality is important but secondary.

For my own part, I assume-until I am provided with enough evidence to suggest otherwise-that commodity prices are likely to remain under secular deflationary pressures for the remainder of the decade, but I cannot be sure. A central banking monetary standard is unsustainable because it is more artificial than a gold standard. I assume, therefore, that another standard (whether better or worse, I do not know) will replace it one day, but I do not know how such a transition would occur. Through a crisis? By accident? It is possible that the current bout of inflation is not, as I suspect, a cyclical deviation from a secular trend but a signal of a breakdown in the system, but I simply do not have any evidence of that, nor do I have a very clear notion of what that evidence might look like.

From the point of view of the history of commodity supercycles, it would be unlikely for commodity prices to remain at their current levels for a sustained period of time. If they do, or if they continue to rise to new highs, that could be a crucial piece of evidence that the monetary system is imploding/exploding. If that happened, expect chaos across markets and social order. The events of the last 22 years have made both the power and fragility of financialized, technocratic globalization apparent.

In short, trading commodities on the basis of a belief in stable supercycles alone would be dangerous. History shows that they can be stable for centuries and then they are not.

A more stable relationship is that between the earnings yield and real commodity prices. The problem here is identical to the one mentioned earlier; once stock prices are treated as a fundamental determinant of commodity prices, assumptions about the “rational” role of supply and demand and the “irrational” role of hopes and fears of buyers are disrupted, perhaps beyond repair. The only way to protect those cherished assumptions is to insist that the connections between commodity prices and the earnings yield are merely coincidental.

Microeconomic investing ramifications

In Part 3, I attempted to show that disruptive innovations emerge near the trough of Kondratiev Waves and mature as the peak approaches, much as Schumpeter argued a century ago. In plain English, they tend to emerge when real commodity prices and equity yields are low and global political stability is high. In the 1000+ pages of Business Cycles, Schumpeter tried to trace the evolution of disruptive innovations and track their interaction with and within an overarching Kondratievian framework. I have avoided doing that with the disruptive innovations of the last century largely because of the time it would take.

According to Econlib, Schumpeter broke technological waves down into three parts:

- 1. Invention (conceiving a new idea or process),

- 2. Innovation (arranging the economic requirements for implementing an invention), and

- 3. Diffusion (whereby people observing the new discovery adopt or imitate it).

The Handbook of the Economics of Innovation describes Schumpeter’s three phases as follows:

According to [Schumpeter’s]…definition, invention concerns the original development of some novel would-be process of production or product while innovation entails its actual introduction and tentative economic exploitation. Diffusion describes its introduction by buyers or competitors….The invention is often introduced from the start as an innovation by economically minded research establishments. Diffusion entails further innovation on the part of both developers and users.

Based in part on a paper called “Invention as a combinatorial process: evidence from US patents“, I am going to slightly reframe this formulation. The authors of that paper say, “A new invention consists of technologies, either new or already in use, brought together in a way not previously seen.” So, first there are technologies or discoveries-something like Eureka moments-that, when combined with other forms of knowledge, can then be turned into inventions. Inventions are then produced and sold, and, once they reach a certain threshold, are then differentiated and improved.

To put a twist on Peter Thiel’s conception of Zero to One, think of “Zero” as being a wholly new idea, “One” as being a new invention, and “Ubiquity” as being mass adoption. It might be better to differentiate “invention” and “innovation” as well, where innovation is the stage at which an invention has the proper configuration of technologies and markets to make it ready for mass diffusion. For example, if the car was invented in the 1880s, the innovations necessary for mass diffusion may not have been in place until somebody like Ford pieced them together and likely involved a total consideration of production, design, cost, and consumption needs. The difference is between that of an inventor and an entrepreneur.

I have found that the following model appears to describe the stages of each of the innovations covered in this series, even if the numbers are not intended to be precise markers.

1. Zero: new technology (Growth: 0/0 vs Diffusion: 0/100)

2. One: a new invention/innovation based on a new combination of technologies (Growth:1/0 vs Diffusion: 1/100)

3. Few: explosive growth and standardization (Growth:10/1 vs Diffusion: 10/100)

4. Many: declining growth rate but accelerating market share (Growth: 50/10 vs Diffusion: 50/100)

5. Ubiquity: mass adoption and differentiation (Growth: 100/50 vs Diffusion: 100/100)

The Kondratiev Upswing tends to occur during Stage 2 and the Peak during Stage 3. Stages 4 and 5 tend to occur during the Kondratiev Downswing.

The question this raises, I think, is, is there a way to identify these innovations when they are still in the cradle, or more broadly, at what point can we identify these disruptive innovations with a reasonable degree of certainty, and how do we exploit those opportunities?

Let’s take the current innovation wave. I have suggested that smartphones are the core consumer durable in this cycle. The first smartphones, depending on when exactly you want to mark their birth, were sold around the turn of the millennium. Apple’s iPhone was not sold until 2006. The standardization of an innovation near the peak of a Kondratiev Wave (in this case, roughly 2010) appears to be typical. If so, that makes it tremendously difficult to anticipate a winner at the trough of the Wave, when these disruptive innovations are first starting to sizzle.

This late standardization appears to have been the case with railroads in the 1860s-1880s. Christopher Gabel wrote an interesting booklet entitled Rails to Oblivion: The Decline of Confederate Railroads in the Civil War for the US Army’s Combat Studies Institute. He was primarily interested, it appears, in dismantling the conventional wisdom about a standardized Northern railway system in contrast to a Southern hodgepodge and the role this contrast played in the War. As part of the argument, he suggests that standardization of US railroads did not occur until the 1870s and 1880s, including in the North.

This appears to have been true of Ford’s role in the early automobile industry. His innovations became the standard rather late in the innovation wave.

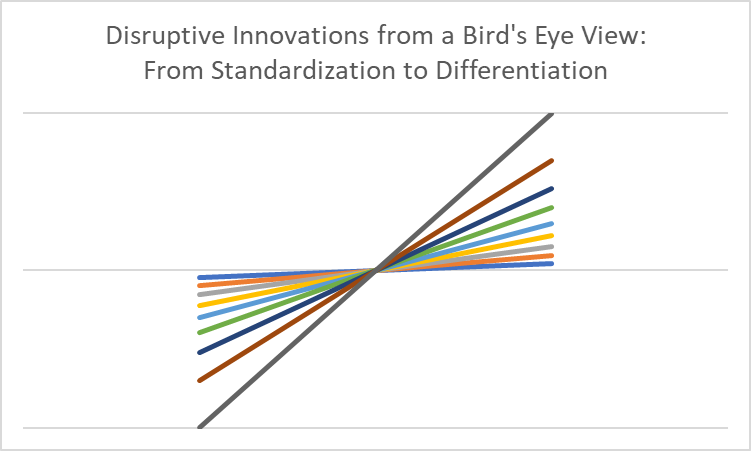

Chart I. The transition from standardization to differentiation occurs near the Kondratiev Peak. (Author)

It would require a Schumpeterian effort to be sure if this pattern has held true across all of the disruptive innovations reviewed in this series, but it appears to be the case that during the Kondratievian Upswing (and probably is the case with all new product-classes), there is not only high growth but extreme competition to be the standard-bearer.

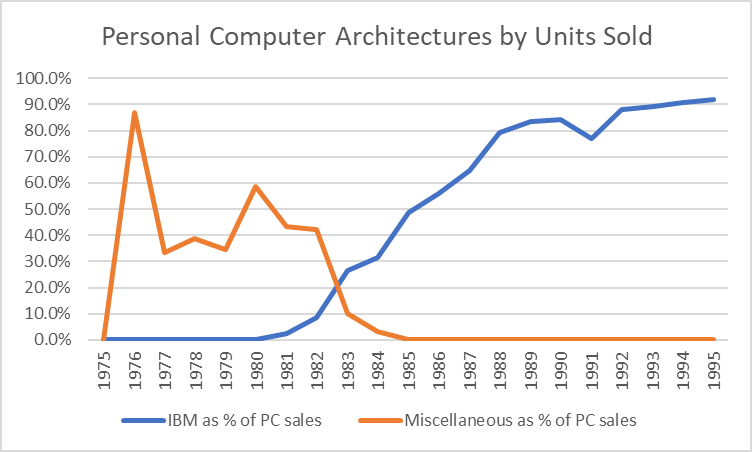

Chart J. The standardization of PCs occurred shortly after the Kondratiev Peak circa 1980. (Wikipedia)

Once standardization occurs, somewhere near (slightly after?) the Kondratiev Peak, differentiation then takes over. Thus, Sloanism soon displaced Fordism in the 1920s.

Color TVs suddenly took over the market in the 1960s, as we saw in Part 3. Standardization of color TV technology seems to have taken place in the early 1950s under the domination of RCA. AmericanBusinessHistory.org says, “At first, RCA held as much as 70% of the market for color television sets, but the other producers quickly joined the fray. By 1964, RCA’s share fell to 42%, followed by Zenith at 14%.” It was not long until RCA was a shell of its former self.

Much the same happened to IBM’s dominance of the PC space in the subsequent Kondratiev/Schumpeter Wave.

So, can we use these patterns to invest?

We have to keep the end in mind to some degree. In the 1920s, GM and RCA’s stock exploded upwards, only to be hit the hardest in the subsequent selloff of the Depression. As I have written in previous articles, consumer durables were part of the tech boom of the 1920s and the tech bust in the 1930s. Yet both GM and RCA survived to play a role in the next boom, even if RCA’s stock did not recover until the 1960s. Ford, as far as I am aware, was not taken public until decades later.

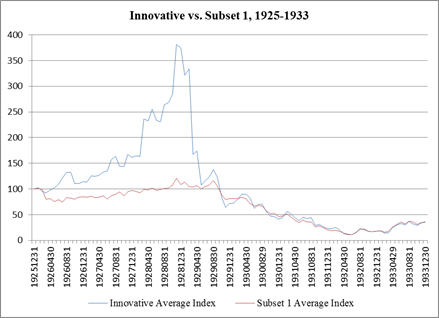

The following chart from an article called “The Stock Market Boom and Crash of 1926-1933: An Applied Time Series Investigation” shows an unweighted stock index composed of innovative companies compared to a broad, unweighted index of companies (“subset 1”) in 1926-1933. The innovative companies included were RCA (radios), Union Carbide and Carbon Corporation (chemicals, auto-related), Dupont (chemicals), and GM (autos).

Chart K. Innovation stocks were hammered by the Great Depression. (Wuthisatian, Papadovasilaki, Gulati, Guerrero)

By 1933, these innovation stocks were a fraction of their 1925 values. But, this only confirms what we have said thus far about the relationship between stock prices, especially tech stocks, and innovation waves. The relationship has to be mediated by the earnings yield and the level of earnings.

The question we really want to ask, I think, is whether we can find the beginning of the thread in real time. I am skeptical, not only for the reasons just mentioned regarding the late standardization of a given innovation, but because even as standardization is occurring, rather deep in the innovation cycle, the people who are best positioned to know often seem to be unaware of the full import of what is happening.

Take Steve Jobs and the iPhone. According to some, Jobs thought the iPhone was just a cellphone. “Jobs, while undeniably brilliant, was not a technological soothsayer who predicted our digital future. He was just trying to make a really cool phone.”

As late as a decade ago, the disruptive technology was supposed to be 3D printing. I say “late”, because according to the schema laid out in this series, the genuinely disruptive technology, the smartphone, was essentially mature while speculation about other technologies abounded. This seems to have been true for Google Glass. The technologists are as unsure as the rest of us are.

Just over 20 years ago, right around the time we ought to expect new disruptive innovations in the consumer durable space, the Segway came out, a “technological marvel…that doesn’t make any sense”, as Wired later put it.

My impression is that knowing when waves of disruptive innovations begin does little to position the general investor to invest in such innovations or the companies or entrepreneurs that create them. Even if one had known that it would be smartphones that would lead the next innovation wave, none of the early smartphone designs survived.

This problem appears to have been magnified with PCs. Software and internet companies were ultimately the prime beneficiaries of that innovation, not computer manufacturers.

If Kondratiev/Schumpeter Waves are not very much use in anticipating which companies or innovations are going to prove to be the big winners in any particular wave, they may be somewhat more useful at the macro level, i.e., the broader market and particular sectors and (perhaps) industries.

Market booms and disruptive diffusions

I have attempted to show that stock market booms tend to begin at the transition from a high-growth/low-diffusion regime to a low-growth/high-diffusion regime in a disruptive consumer durable innovation cycle, but the biggest winners may or may not be directly tied into the production of that innovation.

Stocks seem to react less to the emergence and growth of a disruptive innovation than to the emergence of an ecological system around that innovation. The software on our phones; the data being collected on us; the storage, security, and analysis of that data; the transformation of it for marketing purposes; and so forth. The internet, not the PC. The bungalow; the culture of suburbia; the mall; new fashions, music, and mores; not the automobile or the radio.

Perhaps what distinguishes a run-of-the-mill innovation from a disruptive innovation is that the latter is almost always a physical, durable platform or trellis for subsequent innovations. It provides the physical, consumer-level infrastructure for a total ecological system that will interpenetrate and ultimately subordinate it. (If the car created the suburb, the suburb then made the car indispensable, which is why we are trying to rebuild the energy architecture from scratch rather than re-urbanize city cores). That ecological system cannot truly function until mass adoption occurs. That mass adoption, in turn, coincides with a secular decline in the earnings yield, normally under the power of rising stock prices but sometimes via a deflationary collapse.

If it is true that Steve Jobs did not anticipate what the smartphone would soon become, then the smartphone itself as we know it today was an accidental adaptation to untapped potential of mobile telephony as a vector for internet communication. “Accidental” is not quite the right word, however, since in hindsight, the emergence of the smartphone as we know it seems have been so powerful as to have been virtually inevitable.

In Part I, I presented the following chart as a way of thinking about the emergence and diffusion of disruptive innovations.

Chart L. Disruptive innovations tend to start brewing in the transition from one innovation regime to another. (Author)

While one innovation regime is diffusing, another technology, part synthesis and part antithesis of that regime, is gestating. For unclear reasons, these technologies start giving birth to what are probably batches of disruptive innovations at the bottom of Kondratiev Waves, but these batches are often dominated by one or two core innovations (the smartphone strikes me as being more essential than any given software platform, for example). Once these innovations are standardized with the help of early adopters, they diffuse across societies and form new economic and social configurations at both the macro- and micro-levels. New dreams, new aesthetics, and new morals rise in response. New fears, new hatreds, and new tyrannies, as well.

At each moment, social, political, and economic phenomena are interpenetrating one another and the technological-innovative process. None of these things happen in a vacuum. Elon Musk’s technological aspirations appear to be driven in no small part by his grander aspirations to halt climate change and spread consciousness throughout the galaxy. I cannot help but think that the revolution in gender identities has been facilitated by the rise of gaming and social media and their fostering of an environment in which identities are experimental and malleable.

New fears and new aspirations encourage both innovation and conflict.

Wars and rumors of wars

Many of the wars that broke out near peaks of the Kondratiev Waves were not entirely unexpected, but what seems to have caught contemporaries by surprise is the ferocity of the conflicts. In the US, the threat of a civil war fought over the expansion of slavery in the West had been apparent for decades, but when the actual conflict began, many expected a ” short and relatively bloodless” war.

It has been estimated that, in the first month of World War I, 50,000 “war poems” were being written a day in Germany. The expectation of a brief, victorious war was widespread in Europe.

Both before and immediately after the Nazi invasion of Poland, France, the most consequential frontline Allied power, appears to have expected a relatively easy victory. Germany was regarded as internally divided, weak, ineptly led, and internationally isolated, wrote Haim Shamir in “The drole de guerre and French Public Opinion”. There was “unanimous optimism” in France. “The illusions persisted even after the complete destruction of Poland….The allies’ sea blockade continued to be mentioned as a truly decisive factor in winning the war.” “Only stand still and the walls of Jericho will come tumbling down by themselves,” the French thought.

Poland fell in 1939, well after what are now known to have been clear precursors to the Second World War in Europe, for example, the Spanish Civil War (1936-1939) next door and the Italian invasion of Ethiopia, not to mention Germany’s Anschluss with Austria and invasion of Czechoslovakia in 1938. The Pacific War, depending on how one chooses to demarcate it, began with the invasion of Manchuria in 1931, the Second Sino-Japanese War in 1937, or the 1941 attacks around Asia and the Pacific. The Americans and British, I think it is safe to say, failed to grasp the magnitude of the danger until it was too late.

The gradual escalations in Vietnam 20-30 years later that ultimately evolved into an existential crisis for the US and then, another 30 years after that, the easy victory in the Second Iraq War and Afghanistan War followed by a disastrous and controversial occupation seem to repeat these patterns.

The point I wish to make is that in hindsight, history appears to be leading up to these brutal, transformative wars, but at the time, the scope of the approaching conflict and the losses that will be suffered are frequently underestimated.

Take the Second Iraq War. In the 30 years prior to the US invasion, Iraq had a fought a war with Iran, invaded Kuwait, fought a war with a US-led coalition, and was attacked during Operation Desert Fox. US-led forces enforced a no-fly zone and maintained sanctions in the 1990s. A century from now, historians will probably look back on the period and see everything from the First Iraq War until the Second Iraq War as a single historical event and will likely include East African embassy bombings, the Somali intervention, the World Trade Center attacks and the Afghanistan War, as well. But, in 2000, very few people in the US knew that they were already chest-deep into such an event.

In other words, the problem we found with identifying disruptive innovations at some early stage in the arch of their development appears to be repeated in global political order, even when in hindsight there appears to have been ample evidence of a coming catastrophe at the time. And, this is the same problem we find with major turning points in commodity prices and the earnings yield: in isolation and in real time, the turning points are not clear.

There are two solutions to this problem of being unable to see the forest for the trees, in my opinion.

Trees and Forests

Let me preface this by saying, there is no escaping the unpredictability of history. But, that does not mean we cannot try to understand it better and try to prevent the most extreme negative outcomes. Just as we know that a certain percentage of people are going to die of a given cause each year, we still do our best individually to avoid that fate befalling ourselves and others.

My first solution is to continue excavating historical data and events to discover possible connections between innovation, markets, and political order. This is the more Schumpeterian path. In Business Cycles, Schumpeter tried to turn over every stone of economic history in search of those connections. It certainly makes for a difficult read, but it is ultimately thanks to that work that we have as much understanding of the role of innovation and the entrepreneur that we have today.

The second path is more Kondratievian. Step back from the details and try to observe the overall situation. At present, it appears that we are quite near complete diffusion of smartphones, tech stocks have likely reached a generational peak, the threat of a third world war involving nearly every major power in Europe, Asia, North America, and Oceania is rapidly growing, and domestic sociopolitical order in the core capitalist powers is increasingly fragile. This suggests that we are entering, or have already entered, an extended period of disruption.

One problem with this assessment is that, assuming that the regular cyclicality of Kondratiev/Schumpeter Waves is still in effect, we are roughly eight years away from a secular turn towards rising yields and inflation. Another problem is that commodity prices, especially nominal commodity prices, have been rising to levels not especially typical in a Kondratiev Downswing. If prices and inflation remain high, as discussed above, that could signal a more fundamental breakdown in socioeconomic order. But, as explained above, I assume that prices and inflation are going to moderate.

For these reasons, the current overall situation is most reminiscent of the late 1920s, and we might expect continued deterioration of this overall situation over the coming two decades. That means depressed stock returns, volatile commodity prices, and deflationary pressures this decade followed by inflationary pressures in the next, rising probabilities of geopolitical and domestic political violence, and the emergence of new disruptive innovations.

Wild speculations

Where might those disruptive innovations emerge? Earlier, I said that it seemed to be nearly impossible to identify such innovations in real time. But, there appear to be two industries that dominate these innovation cycles the most: communications and transportation. These are always linked with new durable goods platforms.

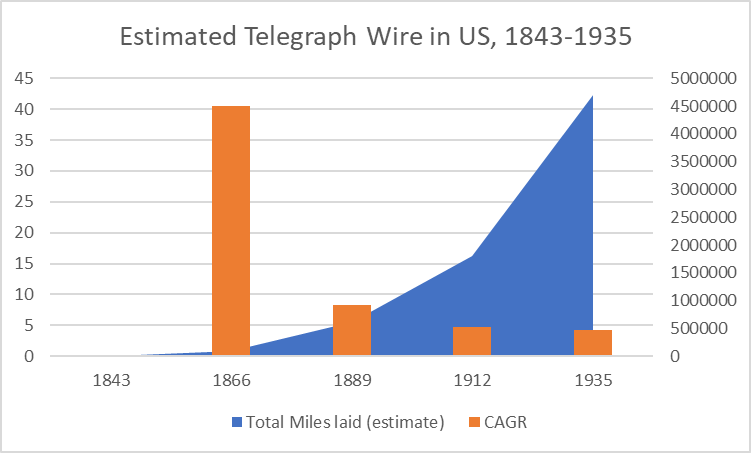

In Part 1, we spoke about the role of railroads in the 19 th Century, primarily because we have good data about them, but the telegraph was perhaps an equally important innovation that appears to have followed the same path of growth and diffusion. The data is somewhat spotty, but it appears that explosive growth in miles of telegraph cable in the 1840s to 1860s was followed by mass diffusion in the subsequent decades. I based the following chart on data from two sources, Elon University’s Imagining the Internet and Cybertelecom.

Chart M. The transition from a high-growth regime to a high-diffusion regime seems to have occurred near the Kondratiev Peak circa 1870. (Imagining the Internet and Cybertelecom; author calculations)

We see the same pattern of growth and diffusion that we have seen in all of the other disruptive innovations, including railroads. High growth in the Kondratiev Upswing and mass diffusion in subsequent decades. We also find the same pattern of standardization near the Kondratiev Peak, this time in the form of industry consolidation (the following quote is from Tomas Nonnenmacher writing for the Economic History Association’s website).

The final phase of integration occurred between 1857 and 1866…By 1864 only Western Union and the American Telegraph Company remained of the ‘Six Nations’[the six largest regional firms]. The United States Telegraph Company entered the field by consolidating smaller, independent firms in the early 1860s, and operated in the territory of both the American Telegraph Company and Western Union. By 1866 Western Union absorbed its last two competitors and reached its position of market dominance.

It seems likely that the next wave of disruptive innovations will also involve communications and possibly transportation. Something like the metaverse could play that role, but that is far from certain. Again, if the claims that Steve Jobs did not fully understand the significance of the iPhone are to be believed, it seems very unlikely that we will know what that innovation is until it is upon us, and even then, we may not quite get it.

What about electric vehicles? It is impossible to rule anything out, but they do not yet appear to bear the hallmarks of being a disruptive innovation, even though they are in the transportation sector. The railroad and the automobile redistributed human populations and industries, or facilitated such a redistribution, across and within geographies. It is not clear that EVs will have that kind of impact, unless it is due to a need to reorganize the energy infrastructure.

If we are really, as a species, going to shift away from hydrocarbons as a primary source of energy, history suggests that will ultimately require more radical transformations than taking an old technology (in this case, cars) and refitting them with batteries. We might have to shift to older patterns of population settlement, for example, denser urban conglomerations built largely on public transportation systems. Without coming to grips with cost disease, especially urban cost disease, that will be extremely difficult.

If we are really going to switch to alternative sources of energy, that will likely lead to a wave of disruptive innovation and creative destruction that we have not seen in perhaps a century. It seems to me unlikely that cars-with-batteries is it. Previous disruptions have always allowed us to do not only more with less but simply more. Genuinely autonomous vehicles might fit the bill, but the closer we get to that goal, the farther away it appears to be.

A meaningful energy transition and/or the emergence of AI would likely constitute Stage 1 technological achievements (effectively, general purpose technologies (or, GPT)) that would give birth to multiple disruptions that would, in turn, create transportation and communication systems unlike anything we currently have before us. It has to be reemphasized that such disruptions would likely ripple through the stock market, the commodities market, and demographics in the nonlinear ways this series has tried to outline. Moreover, these innovation and market disruptions would likely coincide with social disruptions and war.

Conclusion

Over the last 200 years, there appears to have been a consistent relationship across yields, commodity prices, disruptive innovations, and global political stability. Under the gold standard, as first mapped out in the critiques of the capitalist system made by Nikolai Kondratiev and Joseph Schumpeter, long waves rose and fell every 50-60 years and were centered primarily in the production sector. Under a central banking system, those long waves have risen and fallen every 30 years and been centered primarily in the consumption sector. Coincident with that transition from a production economy to a consumption economy has been the transition from an agricultural economy to a service economy and one in which stock prices played a subordinate role to one in which they dominate the long-term movements of the earnings yield.

Even as stock prices dominate the earnings yield, the interrelationships that this series describes also makes it appear that stock prices are an artefact of changes in the earnings yield. Indeed, this is a problem that we come across again and again in a system premised on cross-correlations rather than a clear causative mechanism. This problem is amplified by the fact that the correlations are strongest precisely where they are least likely, for example, in the strong positive correlation between stock prices and the ratio of earnings to commodity prices, which appears to be rooted in centuries’ old relationships.

Thus, as investors, we are presented with a cluster of problems. Without a clear causative mechanism, we can only proceed with caution when using historical patterns to try to anticipate long-term changes, yet these patterns also clearly reject straight-line relationships between “technological progress” and investment outcomes. Periods of high technological growth have often coincided with “secular” bear markets, as in the 1930s, 1970s, and 2000s. Betting on technological growth has only worked consistently for those with extremely long time-horizons (that is, multiple decades).

The long-term solution I recommend is to keep sifting through the rubble of history in search of clues pointing to cause-and-effect relationships but not to embrace any explanation wholeheartedly if it contradicts, by implication, any of the other correlations. I have heard some try to explain the correlation between inflation and yields (usually bond yields but also things like the so-called equity risk premium) as a reflection of the risk high inflation implies, a curious rationalization in a system that is built to burn the world down before it will permit deflation. Yields in the 1920s and 1930s were low, it seems, because it was a low-risk environment.

If you take any of the two relationships we have covered here, you can come up with a nice little theory that appears to explain enough to allow you to pretend the world makes sense. Our reason will happily comply with such storytelling, but history has not complied, and it is unlikely it will change its mind. History, to twist Pascal’s quote, “has its reasons, which reason does not know. We feel it in a thousand things.”

At minimum, any expectations that we have about the future that we extract from our reason should be forced to run through the gauntlet of historical experience before being accepted. If one wants to insist that “this time is different”, that is fine, but it would be necessary to construct an argument that explains why previous patterns and relationships will not hold. Inevitably, history will decide to take a course other than the one it is currently on (and it could be doing so even now), which is why investors ought to keep pondering what the causative mechanisms are and what symptoms a systemic transition might generate. Until a causative mechanism is unearthed or such symptoms appear, it is probably best to assume that historical patterns will persist.

Thus, the historical observations made in this series are most useful for reducing the probabilities of certain outcomes rather than outright predicting. Based on the historical patterns discussed here, it seems unlikely that commodity prices can be sustained at these levels. It seems unlikely that P/E ratios are going to mean revert this decade. It seems unlikely that any disruptive innovations are going to shift towards mass adoption this decade. Based on these factors and patterns described in previous articles, some of which I linked to above, the high returns of the last decade, led by the outperformance of tech stocks, suggests that it is unlikely that they will be able to maintain positive momentum over the coming decade.

That suggests, in this context, that the primary danger to markets is a persistent, deflationary growth shock, which we have not experienced since the 1930s. Finally, all of this suggests that it is unlikely that we will be able to maintain the current level of relative global peace over the next 15-20 years, even if that time is punctuated by periods of de-escalations, rapprochements, and deal-making. At the level of domestic politics (around the world), it is unlikely that we are going to maintain current levels of stability. Typically, volatility rooted in ideological and ethnic strife mixed with class warfare marks such periods. In this total context, transitions in energy systems and demographics would likely help fuel volatility. The silver lining is that over the coming decade, unknown innovators and inventors will likely be coming up with ideas that will help us overcome or bypass some of these problems in the long run. Such innovations are likely to have the potential to make truly profound impacts on our communications and transportation systems and perhaps human consciousness itself. The price for such creativity, however, is a good deal of destruction.

[ad_2]

Source link

More Stories

How To Promote Direct Hotel Bookings

My 50th birthday celebrations in Amsterdam

5 Ways to Improve Hotel Operational Efficiency